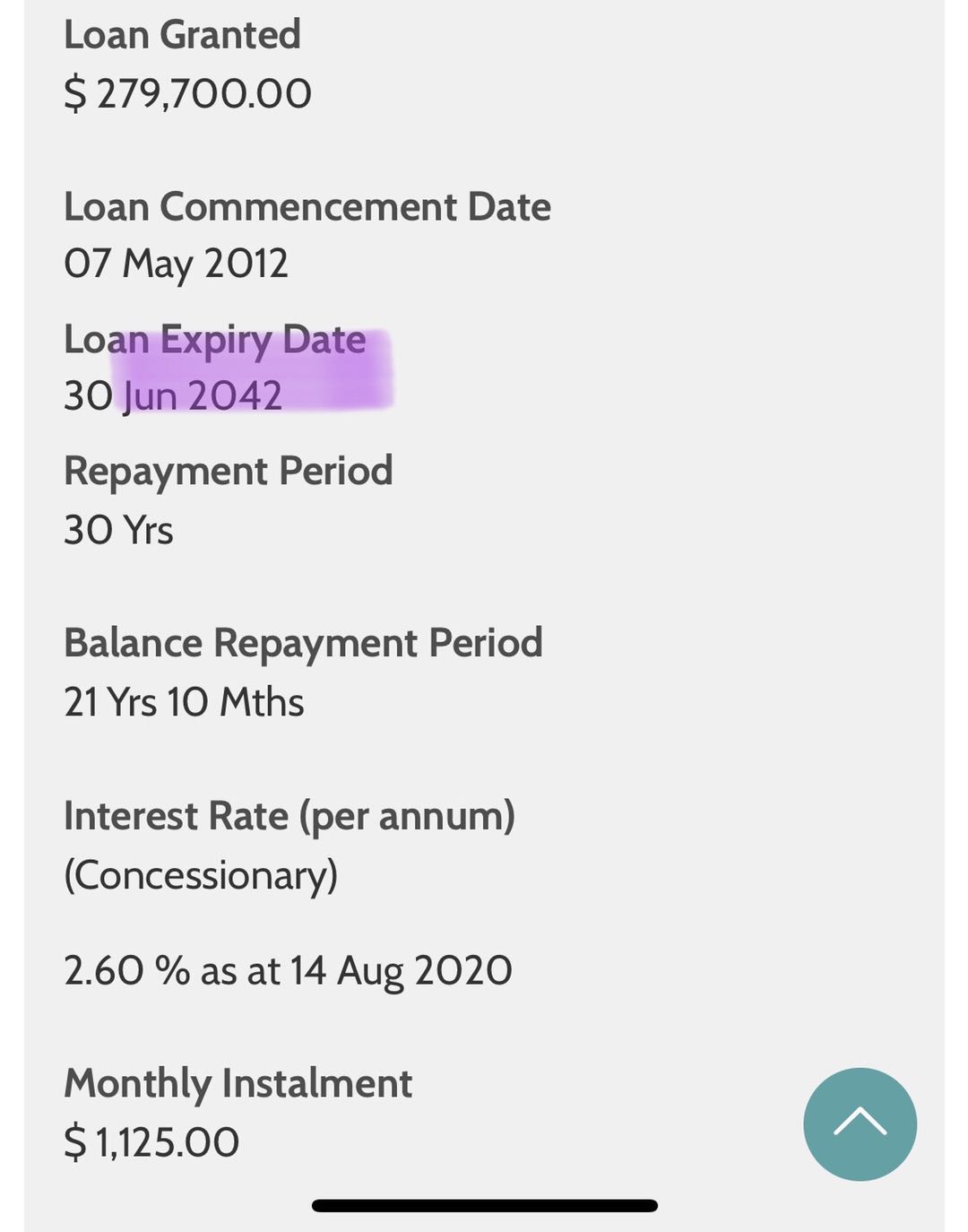

想询问一下关于HDB贷款换银行贷款的refinance

红色彗星 • • 10947 次浏览最近银行的利率确实比较低,找了一个银行的工作人员问大概有1.5左右;其实我目前的房子还有22年月供,房贷剩下22万,拿计算器算了一下如果是拿银行的贷款算来算去每个月大概节省个100块钱;但是银行做re-finance会有2000块钱的手续费,可以用CPF还,加上rebate的1千现金 就是1千手续费;不知道值得不值得做其实我的房贷很少,和几百万的不值得一提,但苍蝇再小也是肉我个人疑惑的是

1. 2年过后利率会调整,到时候浮动利率是个未知数(单据坡县20多年数据银行也没有超过HDB) 到时候再做re-finance 会不会又有一次手续费2. HDB贷款有一点好,毕竟是政府的;如果哪天失业了交不出了房贷,政府也不会收房子,银行就会收回HDB(当年大学教我们法律的老师以前是做律师的,就苦口婆心的给我们说一定要拿HDB贷款)

其实我这点钱就是个渣渣,但自己觉得倒腾倒腾也有点乐在其中;还望有经验的大神解惑。感谢

-

红色彗星 楼主#1

另外我也把Banker发给我的各个银行的利率发出来不过不知道是不是最新的了,如果需要联系方式 可以私信我

HSBC - Floating Rates - 1 Month Sibor as of 9th July is 0.25% - 2 years Lock In

Year 1: 1M SIBOR + 1.05% = 1.30%

Year 2: 1M SIBOR + 1.05% = 1.30%

Year 3: 1M SIBOR + 1.05% = 1.30%

Thereafter: 1M SIBOR + 1.05% = 1.30%

30% partial repayment allowed

One time free conversion to any other packages anytime

Refinancing Legal Subsidy - Below 500K: $1,000 Cash Rebate

UOB - Floating Rates - 3M SIBOR as of 9th July is 0.43% - 2 years Lock In

Year 1 : 3M SIBOR + 1% = 1.43%

Year 2 : 3M SIBOR + 1% = 1.43%

Year 3 : 3M SIBOR + 1% = 1.43%

Thereafter : 3M SIBOR + 1% = 1.43%

Free conversion after 2 year lock in to any other packages.

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

UOB - Fixed Rates 2 year lock in

1st year - 1.40% fixed

2nd year - 1.40% fixed

3rd year and thereafter - ML Board Rate (0.85%) + 0.95% = 1.80%

Free conversion after 2 year lock in to any other packages.

50% Waiver of penalty due to sale of property.

Up to 10% partial repayment allowed per year

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

UOB - Fixed Rates 3 year lock in

1st year - 1.68% fixed

2nd year - 1.68% fixed

3rd year - 1.68% fixed

4th year and thereafter - ML Board Rate (0.85%) + 1.03% = 1.98%

Free conversion after 2 years lock in to any other packages.

Waiver of penalty due to sale of property.

Up to 10% partial repayment allowed per year

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

Maybank - Floating Rates - 3M SIBOR as of 9th July is 0.43% - 1 year Lock In

Year 1 : 3M SIBOR + 0.85% = 1.28%

Year 2 : 3M SIBOR + 0.85% = 1.28%

Year 3 : 3M SIBOR + 1.25% = 1.68%

Thereafter : 3M SIBOR + 1.25% = 1.68%

Refinancing Legal Subsidy - HDB Below 500K - 0.40% of the Loan Amount - Cash Rebate

MayBank - Fixed Rates - 2 years Lock In

Year 1 - 1.50% Fixed

Year 2 - 1.50% Fixed

Thereafter - SRFR2 Board Rates (4.85%) - 2.10% = 2.75%

Refinancing Legal Subsidy - HDB Below 500K - 0.40% of the Loan Amount - Cash Rebate

DBS - Fixed Rates 2 years lock in

Year 1: 1.50% fixed

Year 2: 1.50% fixed

Thereafter: FHR24 - Fixed Deposit Link Rates (0.90%) + 0.90%= 1.80%

Free conversion after 2 years lock in to any other packages.

Waiver of penalty due to sale of property

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

DBS - Fixed Rates 3 years lock in

Year 1: 1.50% fixed

Year 2: 1.50% fixed

Year 3: 1.50% fixed

Thereafter: FHR24 - Fixed Deposit Link Rates (0.90%) + 0.90%= 1.80%

Free conversion after 1 year lock in to any other packages.

Waiver of penalty due to sale of property

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

DBS - Fixed Rates - 5 year lock in

Year 1: 1.50% fixed

Year 2: 1.50% fixed

Year 3: 1.50% fixed

Year 4: 1.50% fixed

Year 5: 1.50% fixed

Thereafter: FHR24 - Fixed Deposit Link Rates (0.90%) + 0.90%= 1.80%

Free conversion after 1 year lock in to any other packages.

Waiver of penalty due to sale of property

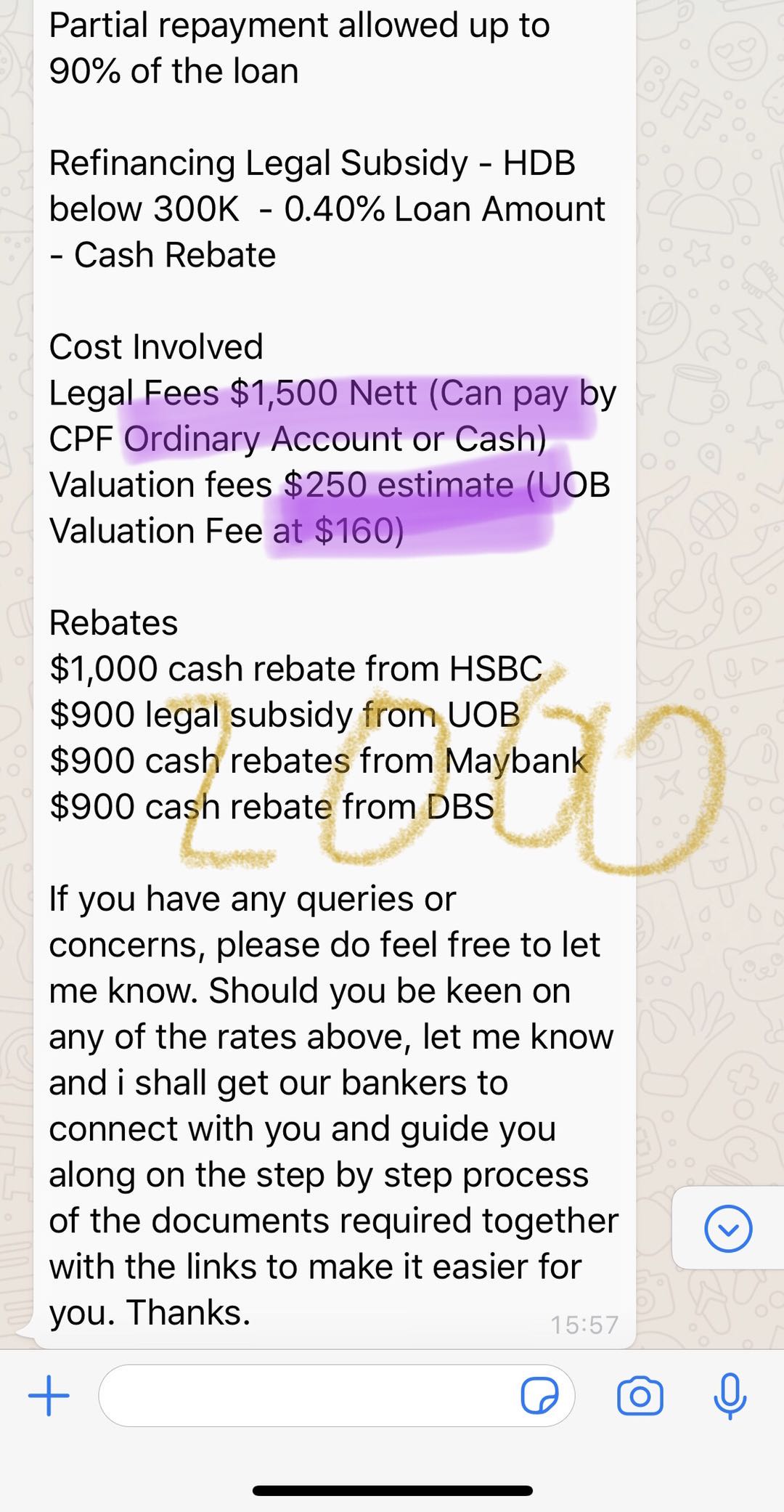

Partial repayment allowed up to 90% of the loan

Refinancing Legal Subsidy - HDB below 300K - 0.40% Loan Amount - Cash Rebate

Cost Involved

Legal Fees $1,500 Nett (Can pay by CPF Ordinary Account or Cash)

Valuation fees $250 estimate (UOB Valuation Fee at $160)

Rebates

$1,000 cash rebate from HSBC

$900 legal subsidy from UOB

$900 cash rebates from Maybank

$900 cash rebate from DBS -

#2

不是很值得主要就是贷款太少。浮动利率未来不知道,所以比较固定利率比较合理。一般在3年内还款,律师费补贴要赔,贷款锁定期内还款也要赔。也就是说一般你要锁3年,利息扣除成本大概省4千,但是你肯定3年内不会卖房子吗?

-

红色彗星 楼主#3

哦 对哟 对哟果然还是网上来问最好,感谢大神

我没有从卖房子来考虑,这是最点醒我了 -

#4

你那教法律的老师太误导人了。HDB可以跟银行贷款从0304年就开始了,如果听他的一年几千十几年小十万块的利息白白浪费了找谁说理去?

-

#5

楼主要先计划一下总共打算在这个房子住多少年

而不是直接拿贷款期22年来算

打算5年后卖了就按5年算

打算3年后直接还清贷款就按3年算

如果啥都没打算那就按15年20年算

这样就能算出来换不换划算不了。算一下吧

-

红色彗星 楼主#6

好的好的 确实这样的思路才是正确的感谢了

-

#7

纯佩服下各种计算不嫌麻烦一直对钱稀里糊涂,典型的我不理财财更不理我( ̄▽ ̄)

-

#8

借贴问一下一般什么情况下才会选择HDB loan啊?

求科普一下和bank loan除了利率、贷款额度年限和提前还款方式以外,还有什么不同啊?

最近纠结要不要拿HDB的loan来付首付,但是利率太高了。。

谢谢~ -

#9

把贷款还清了买第二套把贷款还清了买第二套

-

#10

想太多了 一个月一千来块钱的月供怎么可能交不出来最差的情况你自己睡厅里 房租租出去难道租不到一千?

-

#11

有风险低利率时,选固定利率

高利率时,选浮动利率 -

#12

你贴的这些利率适用于商业地产吗?商业地产啥利率?多谢!

-

红色彗星 楼主#13

商业的是指的商铺那种么估计不行吧,这个利率好像只适合住房贷款的

我毕竟不是专业的,找个银行的Banker问问吧. -

#14

你这个律师费有点贵了啊1.5是五年的固定吧,低的还有1.4%

-

#15

如果短期可能卖房,记得要求waver due to sales