月入6000至2万元者半数入不敷出?

家琪 • • 3424 次浏览-

家琪 楼主#1

神奇的20K再次出现, 谜一样的数字

-

#2

合情合理20k就 贫困线。超过了就能脱贫。

-

#3

huasinger早就给出了说明

-

家琪 楼主#4

不到20K, 永远是入不敷出

-

家琪 楼主#5

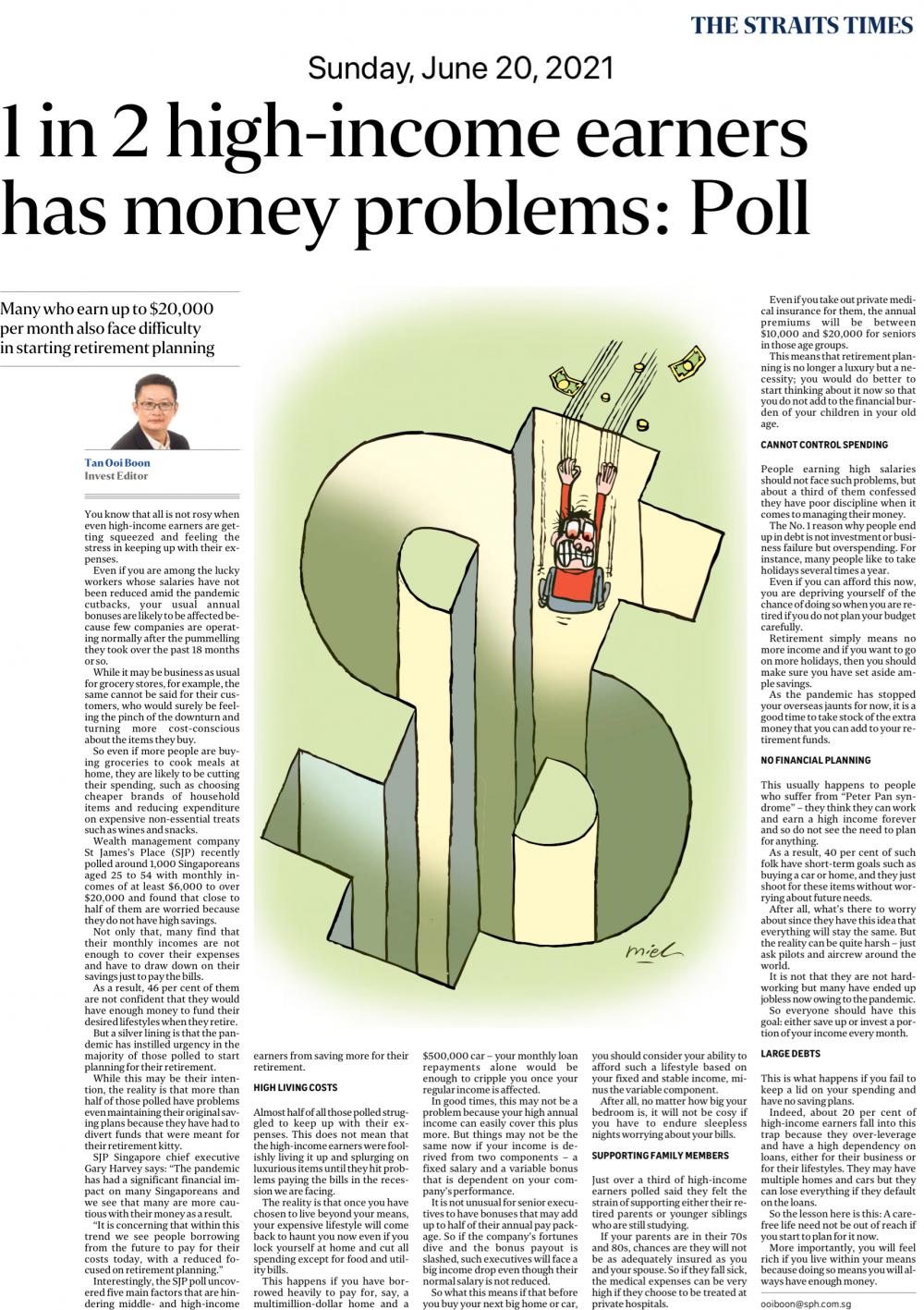

全文A recent poll conducted by a wealth management company St James’s Place Asia (SJP Asia) found that one in two high-income earners in Singapore are facing money issues.

This result was derived from a poll conducted with 1,000 Singaporean respondents aged 25 to 54 with monthly salaries of at least S$6,000 to over S$20,000.

Now the big question is: How are individuals earning almost four times the national median salary still struggling with money problems?

According to data from the Ministry of Manpower (MOM), the median gross monthly income for a full-time employee in 2020 is S$4,535 – which is almost four times higher than S$20,000.

It turns out that being rich and wealthy has less to do with how much you earn, but more to do with what you do exactly with the money you have.

Elaborating further on the financial issues, the poll revealed that the monthly income of these high-income earners is in fact insufficient to cover their expenses, resulting in them having to dig into their savings just to pay the bills.

Given that they have to take out funds from their savings just to pay for their monthly expenses, 46 per cent of them revealed that they don’t have the confidence that they have enough cash to support their desired lifestyle once they retire.

However, there is a sense of urgency in them now to start planning for their retirement.

Although this is their plan, in reality more than half of those polled have problems just maintaining their original saving plans as they have had to redirect funds that were meant for their retirement days due to the current pandemic.

“The pandemic has had a significant financial impact on many Singaporeans and we see that many are more cautious with their money as a result,” said SJP Singapore chief executive Gary Harvey.

He added, “It is concerning that within this trend we see people borrowing from the future to pay for their costs today, with a reduced focused on retirement planning.”

The poll also discovered five main factors that are stopping middle-and high-end income earners from saving more for their retirement.

High living cost

The poll found that the first factor that is stopping these individuals to save up for their retirement is their high living costs. SJP reported that almost 50 per cent of survey respondents struggled to keep up with their expenses.

This is not necessarily because high-income earners splurge on luxurious items during the current recession, but rather about how once they choose to live beyond their means, their expensive lifestyle will come back to haunt them even if they are staying at home and cut all spending except for food and utility bills.

For instance, if they have monthly loan repayment for their multimillion-dollar home and a S$500,000 car, they will find it extremely difficult to pay back these loans when their regular income is affected.

The need to support family members

Over a third of high-income earners who were surveyed felt that they find it an added burden to support their family members – either their retired parents or younger siblings who are still studying.

For parents who are in their 70s and 80s, there are high chances that they’re not adequately insured. This means that if they fall sick, the medical expenses can be very pricey, especially if they choose to be treated at private hospitals.

Another factor is that a third of high-income earners who polled admitted that they cannot control their spending and have poor discipline in money management.

Failure to control spending

Another factor listed in the poll is that a third of high-income earners admitted that they cannot control their spending and have poor discipline in money management.

The main reason why people end up in debt is not due to investment or business failure but overspending, the poll stated.

While these individuals can afford to purchase items that they desire now, but if they fail to plan their budget carefully, chances are they might not be able to much such expensive purchases upon retirement as they have will not be getting their salary anymore.

Poor financial planning

The fourth factor is poor financial planning and this usually occurs to those who suffer from “Peter Pan syndrome”, which basically means that they think they can work and earn a high income forever and don’t see the need to plan for anything.

Due to this, 40 per cent of such individuals have short-term goals like buying a car or home and just focus on such goals without worrying about other future needs like retirement.

Large debts

Lastly, the poll by SJP discovered that high-income earners have large debts, resulting in them facing money issues.

In fact, around 20 percent of those polled over-leverage and have a high dependency on loans, either for their business or for their lifestyles. -

#6

昨天看了一个新闻一个本地高管月薪20k,每个月要给情妇10k,最后把100万的公寓过户给了她。

所以看你怎么花,有了点钱,追求这个追求那个,永远是入不敷出。

一个月2万,要攒100万,也是要不吃不喝五年的 -

#7

哈哈 还是有点不敢相信

-

#8

当然如果是sea大佬 10万股票直接躺变200万,那就另说

-

家琪 楼主#9

请注意用词, 不是情妇, 是甜宝贝,20-21岁的外貌身材姣好的国大女生

-

家琪 楼主#10

国大女生真的很厉害1年赚了很多人10年才能赚的钱

-

家琪 楼主#11

很多人都是超前消费,一个人拿10多张信用卡, 很容易失控

-

家琪 楼主#12

基本消费下表<table>

<tbody>

<tr>

<td><span style="font-weight: 400;">Gift</span></td>

<td><span style="font-weight: 400;">Frequency </span></td>

<td><span style="font-weight: 400;">Total (per year)</span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Basic allowance ($2,500)</span></td>

<td><span style="font-weight: 400;">Once a month </span></td>

<td><span style="font-weight: 400;">$30,000</span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Restaurant dining ($50) </span></td>

<td><span style="font-weight: 400;">3 times a week </span></td>

<td><span style="font-weight: 400;">$7,800 </span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Gold Class movie experience ($42) </span></td>

<td><span style="font-weight: 400;">2 times a month </span></td>

<td><span style="font-weight: 400;">$1,008</span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">VIP concert / festival tickets ($500) </span></td>

<td><span style="font-weight: 400;">4 times a year </span></td>

<td><span style="font-weight: 400;">$2,000</span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Designer handbags, jewellery, gadgets, and etc ($3,000)</span></td>

<td><span style="font-weight: 400;">Once a month </span></td>

<td><span style="font-weight: 400;">$36,000</span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Table service at Marquee (~$4,000 for upper dance floor table) </span></td>

<td><span style="font-weight: 400;">Once a week </span></td>

<td><span style="font-weight: 400;">$48,000 </span></td>

</tr>

<tr>

<td><span style="font-weight: 400;">Sponsored trips overseas ($10,000 + $4,000 travel allowance) </span></td>

<td><span style="font-weight: 400;">2 times a year </span></td>

<td><span style="font-weight: 400;">$28,000</span></td>

</tr>

<tr>

<td></td>

<td><span style="font-weight: 400;">Total</span></td>

<td><span style="font-weight: 400;">$152,808 </span></td>

</tr>

</tbody>

</table> -

家琪 楼主#13

Woah, $152,808 per year is a lot. Divide it by 12 months and it’s about $12,734

-

#14

想当年一个月五百块也是挺过来了。。。

-

家琪 楼主#15

因为那个时候你收入不到6000

-

#16

收入就是五百块啊读大学的时候年收入六千。。。

-

家琪 楼主#17

所以啊, 不是月入6000到20K

-

#18

甜宝贝门槛不高啊。。

-

家琪 楼主#19

主要还是要靠Skill set, 吹拉弹唱什么都要会

-

#20

现在可比以前花的多多了。以前一千块就很好了,现在一万都不够什么。

-

#21

他的意思是,收入低倒不会入不敷出

-

#22

什么样的收入就会有什么样的 living costs.毕竟只有极少数人才有只进不出的生活态度。

-

家琪 楼主#23

低收入的人不是1 in 2, 是 2 in 2

-

#24

菜不够面来凑。

看到就继续努力。 -

#25

陕西土话黑馍多吃菜。

-

#26

哈哈嗯就是这意思~

-

#27

两万家庭挂四十

不高。 -

#28

40同学转发很多。

两万么?有努力么。 -

#29

就没人问过比较打粮食的问题

你怎么赚钱的。 -

#30

百分百心思研究别的。

-

#31

觉得两万很低。换成美金加上税务。

-

#32

或者研究

穷酸的坐怀不乱 -

#33

根本就是很低的工资。

-

#34

职场15年两万是个耻辱。

-

#35

这2万工资也确实剩不下多少,我老公同事10年经验就要这些

-

#36

说起来这么多年这个贫困线也没涨说明其实huasinger在坡县混的越来越差吗。

哈哈 -

家琪 楼主#37

职场15年?? ...这个太严重了

-

家琪 楼主#38

【吐槽八卦】月入6000至2万元者半数入不敷出?

该帖荣获当日十大第2,奖励楼主18分以及27狮城帮币,时间:2021-06-25 22:00:05。该帖荣获当日十大第8,奖励楼主4分以及6狮城帮币,时间:2021-06-26 22:00:41。

该帖荣获当日十大第2,奖励楼主18分以及27狮城帮币,时间:2021-06-25 22:00:05。该帖荣获当日十大第8,奖励楼主4分以及6狮城帮币,时间:2021-06-26 22:00:41。